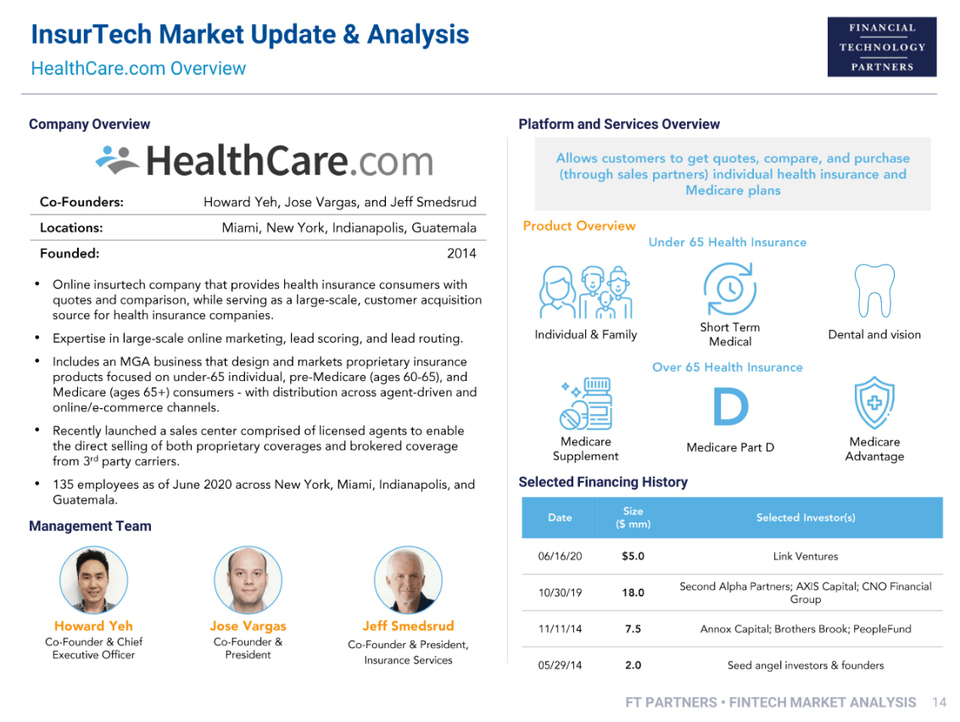

FT Partners CEO Interview: Howard Yeh on Building HealthCare.com and the Future of Digital Insurance Distribution

Howard Yeh is a co-founder of Healthcare.com with two decades of experience building companies in healthcare, insurance, and digital distribution. More about Howard →

.png)

Originally published in the FT Partners CEO Interview Series, July 2020.

What was the vision behind launching HealthCare.com and how has the company evolved over the years?

We started HealthCare.com in 2014 believing there would be a broader shift in consumer health insurance distribution towards digital-native channels. For background, most of our founding team – myself, Jose Vargas, and others – had previous M&A exits together building performance advertising companies driven by our online marketing capabilities.

For this company, we added a new founder, Jeff Smedsrud, who was a health insurance veteran and helped us understand how strategically important the digital channels would become for health insurers, and how they might be acquired by both regulatory and market forces.

Beyond that, Jeff also brought in some new capabilities in designing and developing health insurance coverages and building distribution across direct-to-consumer and traditional broker channels. These capabilities would foreshadow our MGA business a few years after we were founded.

Back in 2014, our initial mindset was simply to get to profitability at scale with a customer acquisition–focused lead generation model. It meant investing in our data infrastructure and online marketing capabilities, and then running a rigorous operation to optimize the levers we had to work with — our campaigns, our conversion funnel, and our lead routing.

We worked with third‑party lead‑demand partners, generally large insurance brokerages or the direct‑to‑consumer divisions of health insurance companies, who would take the consumer from lead to enrollment. That approach was capital‑efficient, asset‑light, and gave us optionality to evolve the business.

What was compelling about the Medicare opportunity for your business?

Our initial interest in Medicare was defensive, especially with shifting regulations and market dynamics in the individual under‑65 market as a result of the Affordable Care Act (ACA). Medicare allowed us to diversify.

Over time, we saw the opportunity become larger for us both horizontally in the addressable market segments and vertically to own more pieces of the customer journey. Three areas where our vision evolved were:

- Diversifying into the senior Medicare segment

- Developing proprietary coverage solutions driven by the acquisition of Pivot Health

- Going deeper into the purchase transaction to complete the data feedback loop

The Medicare market focuses on seniors making individual purchase decisions about how they want to receive their governmental medical benefits. This side of the health insurance market has been stable and growing, with higher lifetime values per sale than the individual under‑65 market.

The growth in Medicare is driven by demographic shifts as the baby‑boomer generation ages into eligibility, and behavioral shifts as digital tools improve. Seniors are increasingly comfortable researching information online, getting quotes digitally, and enrolling with the assistance of modern tools.

Traditional channels such as TV, direct mail, and local agents are still important, but online channels continue gaining share each year.

Given the market sentiment on Medicare, what are your views on the IPOs of GoHealth and SelectQuote?

First, I'm excited for the people behind those companies, some of whom I've worked with for more than a decade. Many of these businesses have been steadily growing for years.

While SelectQuote is a relatively established company in life insurance, its senior health insurance division has grown into the largest part of its business.

Interest in health insurance distribution surged around 2013–2014 with the rollout of the ACA. That enthusiasm cooled after 2015 due to challenges in the ACA market, which pushed many companies to focus more on the senior market and build more predictable growth. That shift is now paying off as investor and strategic interest has returned.

Digitization of insurance distribution has also created concentration at the top. Large national brokerages that can efficiently generate consumer demand have captured increasing market share.

Companies like ours have been able to participate in driving top‑of‑funnel demand. As we build more end‑to‑end sales capabilities, we expect to participate more directly in the value chain.

How does HealthCare.com customize the health insurance shopping experience for each user?

This question goes to the heart of what we do.

As we scaled our lead‑generation business, we realized we were in a position to use far more consumer data signals to create a more efficient path to enrollment.

Because we control both the acquisition sources and the digital funnel, we capture significantly more data than the typical lead.

Examples include:

- Customer acquisition metadata such as search keywords, device type, location, browser, and operating system

- Website behavioral signals including clickstream data and time spent completing quotes

- Consumer responses to preference and intent questions

- Downstream sales outcomes reported by certain partners

We built a proprietary infrastructure to track all of this data and connect it to users, sessions, and conversion events.

That allows us to analyze what happened further down the purchase path — whether we made the right routing decisions and whether a lead was acquired at an appropriate cost. Over time, this helps refine both routing decisions and top‑of‑funnel acquisition strategies.

Does that mean HealthCare.com will migrate to a full end‑to‑end sales model?

We see ourselves as a hybrid.

Our original marketplace model has been successful and we have strong relationships with distribution partners. In many situations routing a consumer to an insurer or broker partner is still the best outcome.

At the same time, developing our own sales capabilities gives us deeper access to data and helps us improve the efficiency of customer acquisition.

So our strategy is to participate in our own marketplace while maintaining strong partnerships across the ecosystem.

What drove the decision to acquire an MGA business in 2018?

Our MGA business, Pivot Health, gives us the ability to design coverage products for underserved market segments.

Pivot Health was founded by Jeff Smedsrud, who originally helped launch HealthCare.com. When we later acquired the business, we saw the opportunity to combine proprietary product capabilities with our direct‑to‑consumer distribution strengths.

Before the acquisition, Pivot relied heavily on external distribution such as call centers and independent agents. Integrating the company allowed us to build stronger direct‑to‑consumer channels and gain deeper insight into enrollment performance and profitability.

Owning products also allows us to analyze claims outcomes and tie them back to acquisition sources. This improves pricing, product design, and targeting strategies.

One example is our Bridge to Medicare solution for consumers aged 60–64 who face challenges purchasing ACA coverage. We continue to introduce new proprietary products designed specifically for direct‑to‑consumer distribution.

How do you plan the business given uncertainty around U.S. healthcare policy?

Change has been constant in the individual health insurance market since the ACA was introduced.

While policy shifts may continue, we focus on building a business that remains nimble and capable of adapting quickly to regulatory changes.

Demand for individual coverage continues to grow as fewer Americans receive traditional employer‑based coverage. Meanwhile, the Medicare market remains relatively stable and continues expanding as the population ages.

Medicare Advantage in particular is growing faster than the Medicare population overall, creating long‑term opportunities in the senior segment.

What trends are driving innovation in health insurance distribution?

In the senior market, digitally native distribution will likely become the dominant channel within the next five years.

However, that does not mean agents will disappear. Agents remain an essential part of the enrollment process, especially when consumers purchase coverage for the first time.

Technology will instead empower agents to become more productive through improved tools, automation, and data insights.

We expect to see continued improvements in self‑enrollment tools, automation, and artificial intelligence that streamline the purchase process while maintaining the advisory role of licensed agents.

Which part of the U.S. healthcare system could be most disrupted by technology?

One area where we expect significant change is price transparency.

Healthcare remains one of the few markets where consumers struggle to obtain clear pricing information before receiving services. As more healthcare costs shift to individuals, transparency will become increasingly important.

Consumers will increasingly expect clearer pricing, easier comparisons, and more transparent coverage information.

What are the company's near‑term and long‑term plans?

Near term, we are expanding our sales center strategy to support end‑to‑end sales for some product lines. Our Indianapolis sales center began 2020 with nine employees and is expected to grow significantly.

Initially we are focused on telephonic sales of Pivot Health products, including short‑term medical plans. Over time we expect sales to become more omnichannel and expand into multi‑carrier offerings including Medicare Advantage and ACA plans.

Looking further ahead, our roadmap includes:

- Expanding proprietary Medicare products

- Building multi‑product Medicare brokerage capabilities

- Strengthening customer acquisition through SEO and paid channels

- Hiring additional technology and data talent

- Enhancing data science capabilities to improve lead routing and conversion

We also plan to continue investing heavily in technology infrastructure, automation, AI, and personalization.

Other areas of focus include expanding self‑enrollment capabilities and increasing lifetime value through cross‑selling and retention strategies.

Despite the challenges of 2020, we view it as an important transition year and a potential inflection point for the company.